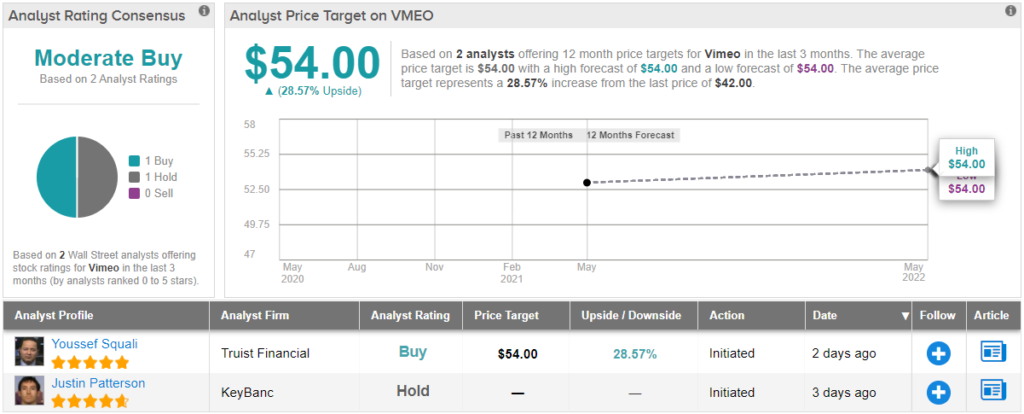

Following in the footsteps of Match Group and Expedia, Vimeo (VMEO) is the latest company to be spun off from Barry Diller’s IAC.The video-software company entered the stock market earlier this week and has made an inauspicious start to life as a public entity, with shares down by 26% already.However, Truist analyst Youssef Squali expects Vimeo to claw back those losses and sees a lot to like about the company often referred to as the “indie YouTube.”Squali initiated coverage with a Buy rating and $54 price target, suggesting upside of ~29% in the year ahead. (To watch Squali’s track record, click here)“We believe Vimeo provides a differentiated offering which caters to both enterprises and self-serve customers,” the 5-star analyst said. “We expect Vimeo to continue to capture share of its large TAM through product innovation and increased enterprise video use cases.”Vimeo is a freemium platform with over 200 million users, and while its business model means it does not generate direct revenue from all its offerings, Squali believes a “vast majority of Vimeo’s value and revenue are built around its tiered priced subscription product.”Using a software-as-a-service (SaaS) model, the subscriptions are sold to businesses and video content producers – anything…

Read More

Vimeo Is Poised for Sustainable Long-Term Growth, Says Analyst